Offshore Staffing for Mortgage Brokers in Australia: How to Scale Loan Processing Without Hiring Locally in 2026

- offshore staffing

- mortgage brokers

- loan processing

- mortgage broker outsourcing Australia

- offshore paraplanning

The mortgage broker channel now accounts for over 74% of all new residential home loans written in Australia, according to the MFAA. That is a record high, and the pressure sitting behind that number is real. Brokers are writing more loans than ever, lender turnaround times remain inconsistent, and the compliance and documentation load under NCCP has not shrunk. What has shrunk is the margin for error and the margin on each deal.

Hiring locally to absorb that load sounds logical until you price it. A full-time loan processor in Sydney or Melbourne will cost you $65,000 to $80,000 per year in base salary, before you add superannuation, leave entitlements, payroll tax, onboarding time, and the very real risk that they leave in 12 months. Most broker principals I speak to are not against hiring. They are against the maths. The return on a local hire, when the hire is positioned purely in a processing and admin role, is difficult to justify at current margins.

Offshore staffing changes that equation. Not because it is cheap labour. Because when it is set up properly, with documented workflows, clear ownership, and a delivery structure built around your business, an offshore loan processor can handle the volume your pipeline demands at a cost that restores your margins and frees you to focus on the work only you can do: client relationships, credit strategy, and growth. This article walks through exactly how that works, what roles you can offshore, what compliance looks like in practice, and how brokers across Australia are already doing it.

Key Takeaways

- Australian mortgage brokers can offshore loan processing, application packaging, lender liaison, CRM management, settlements admin, and paraplanning support without compromising NCCP compliance.

- A dedicated offshore loan processor typically costs 60-70% less than an equivalent local hire when all employment costs are factored in.

- Time-zone overlap between the Philippines and AEST means you get a genuine working day of coverage without relying on async-only communication.

- Compliance risk under NCCP sits with the licensed broker, not the offshore staff member, but your operating model must reflect that with documented SOPs and data handling protocols.

- The difference between offshore staffing that works and offshore staffing that fails is almost always a delivery structure problem, not a talent problem.

- Getting started requires a capacity audit, documented workflows, and a structured onboarding period, not just a job ad and a resume.

Local vs Offshore Loan Processing: At a Glance

| Factor | Local Processor (Sydney/Melbourne) | Offshore Processor (Philippines) |

|---|---|---|

| Annual base salary | $65,000 - $80,000 | $18,000 - $28,000 AUD equivalent |

| Super + leave + payroll tax | Add ~20-25% | Not applicable (managed by staffing partner) |

| Total annual cost | $80,000 - $100,000+ | $22,000 - $35,000 AUD |

| Recruitment timeline | 4-10 weeks | 2-4 weeks |

| Time zone alignment | Full AEST | 2-3 hours overlap minimum, often more |

| NCCP compliance risk | Managed by broker | Managed by broker (same responsibility) |

| SOP dependency | Moderate | High (must be documented) |

| Scalability | Slow and costly | Fast and cost-effective |

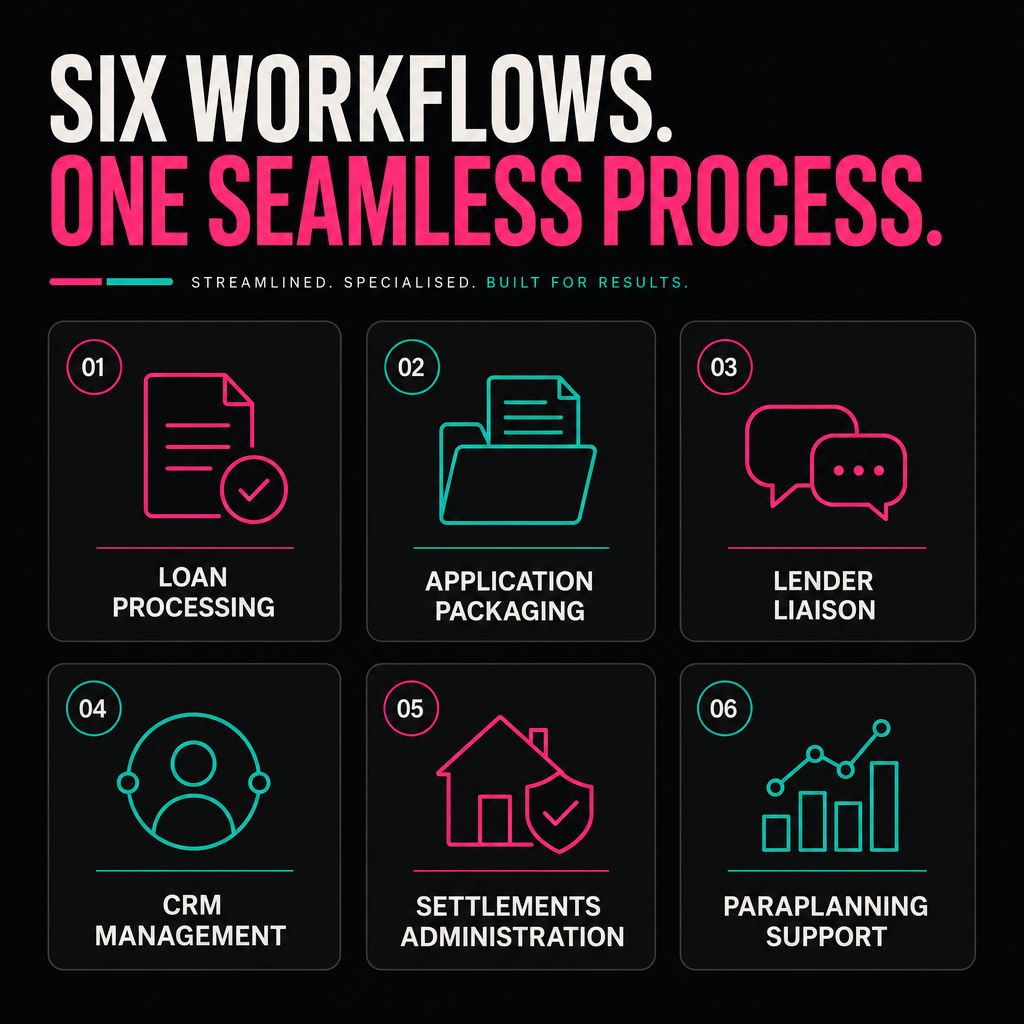

What Roles Can Mortgage Brokers Actually Offshore?

This is the first question most brokers ask, and the honest answer is: more than you think, but not everything. The roles that offshore well are the ones that are process-driven, document-heavy, and repeatable. The roles that must stay local are the ones that require a licensed credit representative to make a judgement call or provide credit advice.

Here is what works:

Loan Processing and Application Packaging

This is the core use case and the one with the clearest ROI. Loan processing involves collecting supporting documents, verifying them against a lender's requirements, completing application forms (in your CRM or the lender's portal), and ensuring the file is submission-ready. An experienced offshore processor who has been trained in your systems and your lender panel can own this end-to-end.

Application packaging is the discipline of presenting a file clearly: income verification, liability schedules, expense summaries, and a clear narrative that supports the credit decision. Lenders approve loans faster when files arrive clean. Brokers who invest in this function, onshore or offshore, see faster approvals and fewer requests for information that stall settlements.

Lender Liaison and Loan Tracking

Chasing lenders for updates is time that earns you nothing. An offshore staff member can own your lender communication queue: following up on application status, responding to lender queries with supporting documents, escalating where needed, and keeping your CRM updated so you and your client always know where the loan sits. This alone can save a broker 8-12 hours a week.

CRM Management and Data Entry

Leads entered late, fact finds not updated, post-settlement tasks missed. These are not strategic failures. They are capacity failures. An offshore team member trained in your CRM (MyCRM, Salestrekker, Connective Essentials, or whatever you use) can handle data hygiene, pipeline updates, task management, and report generation as a standing function.

Settlements Administration

Settlements have their own admin load: coordinating with conveyancers and solicitors, confirming discharge dates, preparing settlement figures, and managing the post-settlement communication to your client. This is high-stakes work with clear process steps. It is documentable, and it is offshore-ready.

Paraplanning Support

For brokers who also hold a financial planning licence or work alongside a financial adviser, offshore paraplanning support is increasingly viable. Preparing research summaries, running product comparisons, building SOA templates, and maintaining adviser file notes are all tasks that a trained offshore paraplanner can handle. This is a growing use case as the lines between broking and holistic financial advice continue to blur.

The Roles That Should Stay Onshore

Credit advice, client-facing needs analysis, strategy conversations, and the signing of credit proposals must remain with your licensed credit representative. This is not negotiable under NCCP. Offshore staff are operational support, not credit advisers. Any provider who implies otherwise is selling you risk, not capacity.

How an Offshore Loan Processor Fits Into Your Workflow

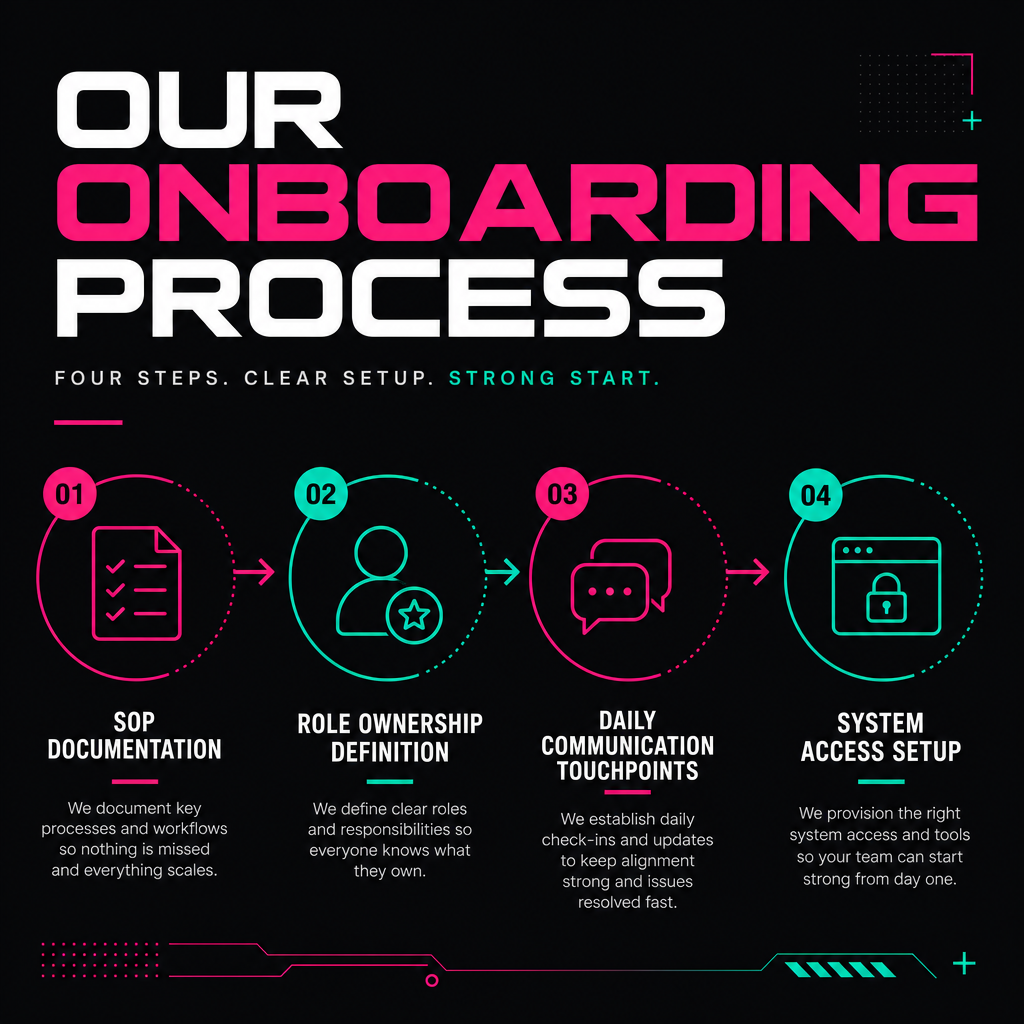

The most common failure mode I see is brokers who hire an offshore processor and then hand them a login and a list of tasks. Two months later they wonder why output is inconsistent. The problem is never the person. The problem is the absence of a system.

An offshore loan processor needs four things to perform reliably:

- Documented SOPs for every task they own. Not a one-page overview. Actual step-by-step process documents that cover what to do, what to check, what to escalate, and where to record the output.

- Clear ownership boundaries. They need to know exactly where their responsibility begins and ends on each file. Ambiguity creates delay and error.

- Daily communication touchpoints. A morning check-in (which lands in your afternoon given the time zone) keeps files moving and issues surfaced early.

- Access to the right systems. CRM access, lender portal logins (within your security policy), document storage, and communication tools.

At Remotee, we work through a structured onboarding period before any offshore hire is handling live files independently. That period covers workflow documentation, system training, shadow processing on completed files, and a review phase before they take ownership. This is not slow. It is what separates predictable delivery from expensive disappointment.

For brokers who want to assess where their capacity bottlenecks actually sit before hiring, the Remotee mortgage broker capacity assessment is a practical starting point.

NCCP and Privacy Compliance: What You Need to Know

NCCP compliance sits with the licensed broker. Full stop. Your offshore loan processor is not a credit representative and does not provide credit assistance. They are an operational staff member supporting your licensed activities. That distinction matters legally and practically.

What this means in practice:

Credit advice stays with you. Your offshore processor can prepare a file, but they cannot tell a client which product to choose or why. Any communication that constitutes credit assistance must go through your licensed rep.

Privacy Act obligations apply regardless of where staff are located. If your offshore team member is handling personal financial information (and they will be), your business must have a privacy policy that covers offshore data handling. The Australian Privacy Principles under the Privacy Act 1988 apply to how you collect, store, and transfer that data. You need to ensure your offshore provider operates with a data security framework that matches your obligations.

Data security is not optional. At a minimum, you should be looking for: encrypted document transfer, role-based access controls, no local storage of client documents on personal devices, and a clear data handling agreement with your staffing provider. Ask specifically whether your provider holds or is working toward ISO 27001 certification. For clients at our end, we build data handling protocols into the onboarding structure, not as an afterthought.

Lender portal access requires care. Some lenders have terms that restrict who can access their portals on your behalf. Review your aggregator's compliance requirements and your lender contracts before giving portal access to offshore staff. In most cases, access under your credentials with clear audit trails is acceptable. But check, do not assume.

For brokers working with an aggregator such as Connective, AFG, or Finsure, check your compliance obligations around offshore staff with your aggregator's compliance team before you start. Most aggregators have existing guidance on this.

Time Zone Overlap: Is It Actually Workable?

This is the concern I hear most often, and it is the concern most quickly resolved once brokers see it working.

The Philippines is in Philippine Standard Time, which is UTC+8. AEST is UTC+10 in winter and UTC+11 in summer. That gives you a 2-3 hour overlap in real business hours when both teams are working a standard day. That sounds thin, but in practice it works because:

- Most loan processing tasks are async by nature. Your processor works through the queue while you are in client meetings. You review output at the end of your day or early the next morning.

- A morning check-in from your offshore processor lands in your late afternoon, which aligns well with an end-of-day review.

- Many offshore staff working for Australian businesses adjust their start times to align better with AEST, extending the working overlap to 4-5 hours when needed.

For time-sensitive lender communication or settlement-day coordination, you build escalation protocols: a clear list of what gets flagged immediately via mobile message versus what goes into the daily update. This is not complicated. It is just a process that needs to be documented.

The Real Cost Comparison

For a full breakdown of offshore versus local hiring costs with worked examples across multiple role types, the offshore vs local hiring cost comparison on the Remotee blog covers it in detail. Here is the short version for loan processing specifically.

A local loan processor in a major Australian city costs $65,000 to $80,000 in base salary. Add compulsory superannuation (11.5% in 2026), annual leave loading, potential payroll tax (if your wages bill exceeds the state threshold), and recruitment costs, and your all-in annual cost sits at $85,000 to $105,000 before you account for management overhead.

An offshore loan processor through a structured provider costs $22,000 to $35,000 AUD per year, fully managed. That includes the staff member's salary, HR management, compliance support, and the delivery infrastructure. The saving is $50,000 to $70,000 per year on a single role.

For a broker writing 15-20 loans per month, one offshore processor covers the processing load. For a broker at 25-35 loans per month, you are looking at two offshore staff, potentially a processor and a settlements admin. Even at two roles, the cost sits well below one local hire.

You can review current pricing structures for Remotee's mortgage broker staffing arrangements at remotee.com.au/pricing.

Two Real Outcomes Worth Knowing

Broker Principal Reduces Processing Backlog by 11 Days

I worked with a broker principal running a two-broker business in Queensland. They were writing 22-25 loans per month and managing loan processing themselves, between client calls. Files were sitting in "packaging" for an average of 8-11 days before submission. By the time the lender received the file, the client had already asked twice what was happening.

We ran a capacity assessment, documented their existing process (which was mostly in one broker's head), and placed a dedicated offshore loan processor with them. Within six weeks, average time from fact find to submission was down to 3 days. Lender turnaround improved because files arrived complete. The broker got back roughly 15 hours a week and used most of it to take on an additional 6 loans per month. That is roughly $36,000 to $48,000 in additional annual commission on their trail book, from a role that cost them $26,000 per year.

Aggregator-Aligned Brokerage Scales to New State Without Local Hire

A mid-sized brokerage with existing operations in New South Wales wanted to expand into Victoria without opening a physical office or hiring locally. The compliance overhead of a new state hire, combined with the cost, made the numbers difficult.

We built an offshore team of two: a loan processor and a CRM and settlements admin. Both were onboarded to the brokerage's Victorian lender panel requirements (which differed from NSW in several respects), trained on their SOPs, and embedded in their Salestrekker workflow. The Victorian expansion reached breakeven in month four. The brokerage is now writing 18 loans per month from Victoria without a single local hire in that state.

I have seen this pattern enough times to say with confidence: the constraint is almost never finding the right person. The constraint is building the system they operate inside.

Getting Started: A Step-by-Step

Step 1: Assess your actual capacity gap. Before you hire anyone, you need to know where time is being lost and what tasks are genuinely process-driven versus judgement-driven. The mortgage broker staffing page at Remotee gives you a clear framework for this.

Step 2: Document your workflows. This step is non-negotiable. If your process for packaging a loan application lives only in your head, you are not ready to offshore it. That documentation does not have to be perfect before you start, but it has to exist. We help clients through this as part of onboarding.

Step 3: Define the role clearly. A job title is not enough. What does the person own? What do they escalate? What systems do they access? What is the daily communication rhythm? What does a well-done day look like? Answer these questions before you hire.

Step 4: Work through a structured onboarding period. The first 30-60 days are about system calibration, not volume. Your offshore processor should be shadow-processing completed files, asking questions, and building familiarity with your lender panel before they own a live pipeline.

Step 5: Build in a review cycle. Monthly at minimum. Review output quality, turnaround times, error rates, and communication. Fix problems at the system level, not by pushing harder on the individual.

If you want to talk through where your brokerage sits and whether offshore staffing is the right next move, get in touch with the Remotee team. We do not push every broker toward offshore hiring. Some businesses are not ready for it. But if you are writing more than 15 loans per month and spending meaningful time on processing, the numbers almost always support a conversation.

References

- Mortgage and Finance Association of Australia (MFAA). Industry Intelligence Service Report. MFAA, 2026. https://www.mfaa.com.au

- Office of the Australian Information Commissioner (OAIC). Australian Privacy Principles Guidelines. OAIC. https://www.oaic.gov.au/privacy/australian-privacy-principles

- Australian Securities and Investments Commission (ASIC). National Consumer Credit Protection Act 2009: Regulatory Guide 209. ASIC. https://asic.gov.au

FREQUENTLY ASKED QUESTIONS

Common questions

Is offshore loan processing legal for Australian mortgage brokers?

- Yes. Offshore loan processing is legal provided the licensed broker retains responsibility for all credit assistance and advice. Offshore staff operate as operational support, not as credit representatives. Your NCCP obligations remain with you as the licence holder. You must also ensure your data handling practices comply with the Australian Privacy Principles, including provisions that apply when personal information is held offshore.

What is the typical cost of an offshore loan processor for an Australian broker?

- Through a structured offshore staffing provider, you are looking at $22,000 to $35,000 AUD per year for a dedicated offshore loan processor. This compares to $85,000 to $105,000 all-in for an equivalent local hire when you include superannuation, leave, payroll tax, and recruitment costs. The saving on a single role is typically $50,000 to $70,000 per year.

How do I handle Privacy Act obligations when using offshore staff?

- You must ensure your business has a privacy policy that covers offshore data handling. The Australian Privacy Principles apply to all personal financial information you collect, store, and transfer, regardless of where staff are located. Your offshore provider should have a documented data security framework, role-based access controls, and encrypted document transfer as a baseline. Ask specifically about ISO 27001 certification and get a data handling agreement in place before any client information is shared.

Will my aggregator allow offshore staff to access lender portals?

- This varies by aggregator and lender. Most aggregators have existing guidance on offshore staff and portal access. Check with your aggregator's compliance team before granting portal access. In most cases, access under your credentials with clear audit trails is acceptable, but the terms of your lender contracts and aggregator agreement take precedence. Do not assume. Check.

How many loans per month do I need to be writing to justify offshore staff?

- As a general guide, 15 or more loans per month is the point where offshore processing starts to show a clear ROI. Below that, the processing load can often be managed with better systems rather than additional headcount. Above 25 loans per month, a single offshore processor may not be sufficient, and you should be looking at a processor plus a settlements or CRM admin role.

How does the time zone difference work in practice?

- Philippine Standard Time is 2-3 hours behind AEST. In practice, many offshore staff working for Australian businesses shift their hours to create a longer overlap. The async nature of most loan processing tasks means your offshore processor works through the queue during their day, and you review output in your afternoon or the following morning. For time-sensitive tasks, you build simple escalation protocols using mobile messaging.

What systems do offshore loan processors typically use?

- Experienced offshore processors who specialise in the Australian broker market are generally familiar with MyCRM, Salestrekker, Connective Essentials, and Apply Online. They can also be trained in lender-specific portals and document management systems. The key is that your system access, permissions, and data handling protocols are set up before the processor starts.

How long does it take to get an offshore loan processor up and running?

- From initial enquiry to a processor working on live files, allow 4-8 weeks. That includes role scoping (1-2 weeks), recruitment and placement (2-3 weeks), and a structured onboarding and shadow period (2-4 weeks). Trying to compress this timeline is one of the most common causes of offshore hiring not delivering the expected results in the first 90 days.

Jon Kelly

Founder, Remotee

Jon helps Australian businesses build compliance-led offshore teams that scale without the burnout. NDIS, accounting, mortgage broking, recruitment and digital marketing.

KEEP READING

Related posts

offshore staffing roles

Which Roles Are Best Suited to Offshore Staffing? A Guide for Australian Businesses in 2026

The most expensive offshore staffing mistake I see Australian business owners make is not hiring the wrong person. It is offshoring the wrong role. They start w…

23 June 2026 · 23 min read

offshore staffing cost

How Much Does Offshore Staffing Cost in Australia? A 2026 Breakdown of Savings and Pricing

Key Stats: Australian employers pay an average of 20-30% on top of base salary in statutory on-costs (superannuation, payroll tax, WorkCover, leave loading). A…

20 June 2026 · 26 min read

hire offshore staff

How to Hire Offshore Staff in Australia: A Step-by-Step Guide for 2026

Hiring offshore is not a leap of faith. It is a decision with a clear process behind it, and the Australian businesses getting real results in 2026 are the ones…

19 June 2026 · 26 min read

READY TO SCALE WITHOUT THE BURNOUT?

Build a compliance-led offshore team in 3–4 weeks.

Tell us about your current bottleneck and we'll show you what a Remotee placement would look like for your operation.

Or get our playbooks emailed to you instead.